NEWS & INSIGHTS

News - June, 2023

Cipio Partners has prospered for twenty years. Time to reflect on the next twenty years of European Technology Investing.

It took European technology well over a decade to rise from the ashes of the internet bubble. Today, the ecosystem seems mature and resilient. What will it take to overcome new challenges and finally be able to narrow the gap with the US and China?

The Covid bubble and the subsequent bust

When the pandemic hit the world in early 2020 nobody knew what the impact on the world of technology companies might be. Very soon though, it became clear that two things were happening.

1) Covid was turbo charging every aspect of the of the ongoing transformation of the economy: video conferencing, cloud computing and the digitization of work. All of these trends accelerated.

2) Loose monetary policy drove interest rates to zero, even negative. The cost of capital became close to zero and valuations of technology companies went through the roof.

Obviously, it could not last. When the pandemic ended, excess liquidity and supply chain issues triggered inflation levels unseen for decades, forcing central banks to raise rates. In Q4 2021 tech valuation started to decline fast.

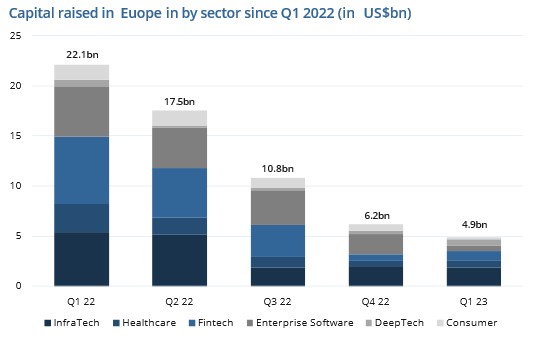

European Venture Capital investments have declined every quarter since Q4 2022. In Q1 2023 investments are down 78% against one year ago. Venture Capital fundraising is fairing equally poorly.

Source: Lazard VGB Insights, Pitchbook Data Inc

The down market is more comparable to 2001 than to the Global Financial Crisis. Rising interest rates not only push tech valuations down, but they also lead to capital flowing away from technology into other areas of the economy. Owners of technology assets are keen to sell, and yet again, demand for secondary transactions is rapidly rising.

How will European technology fare after its second major crisis?

It depends. It is entirely possibly that a replay of the old narrative of “European technology doesn’t work” will take hold. Limited partners would withdraw, government would reduce funding, technology firms would close and people would go back to the “old economy” – just as it happened 20 years ago.

However, we at Cipio Partners are optimists. We at Cipio believe this time it is different. We believe that European entrepreneurs and European investors have proven over the last 10 years that European technology does “work”. Europe has created some major entrepreneurial success stories such as Spotify, Adyen, Booking, King, and 150 other European Unicorns (1). European investors have made money. Just as nobody in the US lost faith in 2001, and nobody is losing faith today, there is no reason for anybody in Europe to lose faith in the ability of the technology industry to create value.

So, what’s the playbook for bouncing back?

- Courageously move to the next big thing: The unicorns and decacorns in 5-10 years will come from new sectors. We need to move courageously into these new sectors: Quantum Computing, AI and Machine Learning, Synthetic Biology, decarbonization of all industrial processes and many other areas. Europe has some strong technology in these areas. Europe has ample and relatively inexpensive engineering talent. But we need to take more risks and start and fund more companies in the industries of tomorrow.

- Get a bigger boat: To build ambitious companies in the sectors mentioned above, we need much bigger amounts of funding. US and Chinese firms can access such capital, because local venture and growth funds are much bigger. We need such bigger funds in Europe. More government money is nice, but it is not really the best solution. What we need is to liberate the very large pool of capital that are today stacked away in insurance companies and pension funds earning minimum returns from fixed income and real estate. We need to redirect these funds into a new breed of much larger growth funds, that can invest in ambitious companies at the appropriate scale.

- Attractive capital markets: Europe not only needs to build the next generation of unicorn and decacorn technology businesses, but it needs some of these businesses to remain independent, continue to scale and become aggregators of smaller European tech firms. Such companies can only live on a capital market of scale, that today doesn’t exist in Europe. Euronext and Deutsche Börse should merge and create a dominant pan-European stock exchange. We need to bring back technology analysts, review regulation and fiscal rules to make such a technology stock exchange a model of transparency and good governance to create the best possible conditions for global investors to put their money here.

Conclusion

Europe’s first incarnation of its own technology industry, the internet startups created in the late 1990s, was largely a failure. When a cyclical downturn hit the industry, people lost faith, funding dried up and few businesses of scale survived. European technology had to wait over ten years before it had its second chance.

Over the past ten years courageous entrepreneurs and investors rebuilt the European technology industry from scratch. It cannot quite rival the US, nor China, but it is a player. This achievement is at risk again in the downturn triggered by war and inflation. In the face of the current challenges, we need to build on our strengths, double down on the past achievements, take risks on new sectors, make dramatically more capital available for scale-ups and build more attractive capital markets for the European decacorns of tomorrow.

And again, just as 20 years ago, Cipio Partners will be there.

Sources:

Image by Ina Zabel: Diana Meyel, Roland Dennert and Dr. Hans-Dieter Koch

(1) Sifted